Woolworths increases lead in $100b+ grocery war

The latest results from Roy Morgan show that in the 12 months to December 2017, Woolworths has 32.2% of the total grocery market (including fresh food), an increase of 0.8% points over the 2016 result. The Coles Group achieved 28.8% share, up by only 0.1% point.

These results are from the Roy Morgan Single Source survey of over 50,000 people per annum, including over 12,000 grocery buyers.

Aldi and Woolworths show greatest gains in market share

The two best performers in 2017 for gaining share in the total grocery market were Aldi, up 0.8% points to 12.1% and Woolworths up 0.8% points to 32.2%. This now makes the combined market share of Woolworths, Coles and Aldi 73.1%, up 1.7% points over last year. IGA appears to be struggling in fourth place on 7.4%, down 1.1% points for the year.

Non-supermarket food retailers such as butchers, fruit shops, markets, and convenience stores currently have 11.8% market share, but are showing some weakness over the last year, being down by a combined 0.8% points.

Share of Total Grocery Market1

Source: Roy Morgan Single Source. 12 months ended December 2016, n = 11,613; 12 months ended December 2017, n = 12,313. Base: Grocery buyers aged 14+. 1. Includes fresh food

Fresh food a highly competitive area for supermarkets

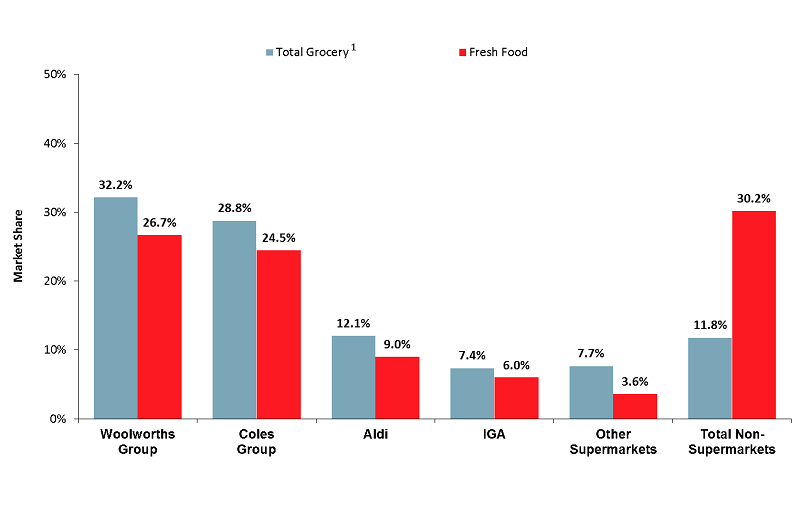

All of the major supermarkets have a lower market share of the fresh food market than their overall grocery market share. This is a result of the specialty retailers that compete in the fresh food segment such as bread shops, fruit shops, butchers, seafood retailers etc. The best performers in this segment are the non-supermarket group with 30.2% share, followed by Woolworths (26.7%), Coles (24.5%) and Aldi (9.0%).

Share of Total Grocery Market1 vs Share of Fresh Food Market

Source: Roy Morgan Single Source. 12 months ended December 2017, n= 12,313. Base: Grocery buyers aged 14+. 1. Includes Fresh Food.

Lack of loyalty among supermarket shoppers

There is clearly a lack of loyalty when it comes to supermarket shopping with very few customers only shopping at one supermarket. An example of this is that although 72.7% of grocery buyers shop at Woolworths, a much lower 8% shop only at Woolworths. It is a similar situation with Coles shoppers, where 70% shop but only 6.6% shop exclusively. The store overlap in shoppers of the big 2 is very large with over half of them shopping at both Coles and Woolworths.

Norman Morris, Industry Communications Director, Roy Morgan says:

“The recent announcement by Wesfarmers to demerge Coles is likely to result in increased pressure in this highly competitive $100b plus grocery market. When Coles becomes listed on the ASX, it is likely to lead to increased analysis and pressure on their financial results and the obvious comparison with Woolworths.

“Woolworths currently appears to have an edge over Coles but both are facing increasing competition from Aldi and the arrival of others including Kaufland and Lidl that will put even more pressure on this market. Lack of loyalty among supermarket shoppers that we have seen in this release presents both a major opportunity for current players to gain customers but also a good environment for new entrants to build a customer base like we have seen with Aldi.

“The current aim of the major supermarkets to be positioned as being strong in ‘fresh food’ is a result of it being seen as an area of major growth potential. This market is very significant, with an estimated annual turnover of over $40b or nearly 40% of the total grocery market. The smaller specialist retailers or non-supermarkets mainly operate in the fresh food area and include fruit shops, butchers, bread shops etc. Together they currently hold a 30.2% of the fresh food market or 11.8% of the total grocery segment but appear to be losing market share to the majors.

“This analysis is from the extensive Roy Morgan Supermarket & Fresh Food Currency Report which covers all food retailers, including products purchased and dollars spent. The combination of the large annual sample collected over more than a decade enables a unique in depth trend analysis of this very significant market.”

For comments or more information please contact:

Roy Morgan - Enquiries

Office: +61 (03) 9224 5309

askroymorgan@roymorgan.com

Margin of Error

The margin of error to be allowed for in any estimate depends mainly on the number of interviews on which it is based. Margin of error gives indications of the likely range within which estimates would be 95% likely to fall, expressed as the number of percentage points above or below the actual estimate. Allowance for design effects (such as stratification and weighting) should be made as appropriate.

| Sample Size | Percentage Estimate |

| 40% – 60% | 25% or 75% | 10% or 90% | 5% or 95% | |

| 1,000 | ±3.0 | ±2.7 | ±1.9 | ±1.3 |

| 5,000 | ±1.4 | ±1.2 | ±0.8 | ±0.6 |

| 7,500 | ±1.1 | ±1.0 | ±0.7 | ±0.5 |

| 10,000 | ±1.0 | ±0.9 | ±0.6 | ±0.4 |

| 20,000 | ±0.7 | ±0.6 | ±0.4 | ±0.3 |

| 50,000 | ±0.4 | ±0.4 | ±0.3 | ±0.2 |