Inflation Expectations up 0.2% points to 5.9% in July – the highest monthly rating for eight years since August 2012

In July 2022 Australians expected inflation of 5.9% annually over the next two years, up 0.2% points from June 2022 and the highest Inflation Expectations have been for eight years since August 2012.

Inflation Expectations in July are a large 1.8% points higher than a year ago in July 2021, and 2.5% points above the near record low of 3.4% in July 2020. Inflation Expectations were at 5.8% in March but plunged in April and May to 5.3% after former Federal Treasurer Josh Frydenberg cut the petrol excise in half – a cut of about 25 cents per litre – but the measure has now quickly rebounded back above its recent high.

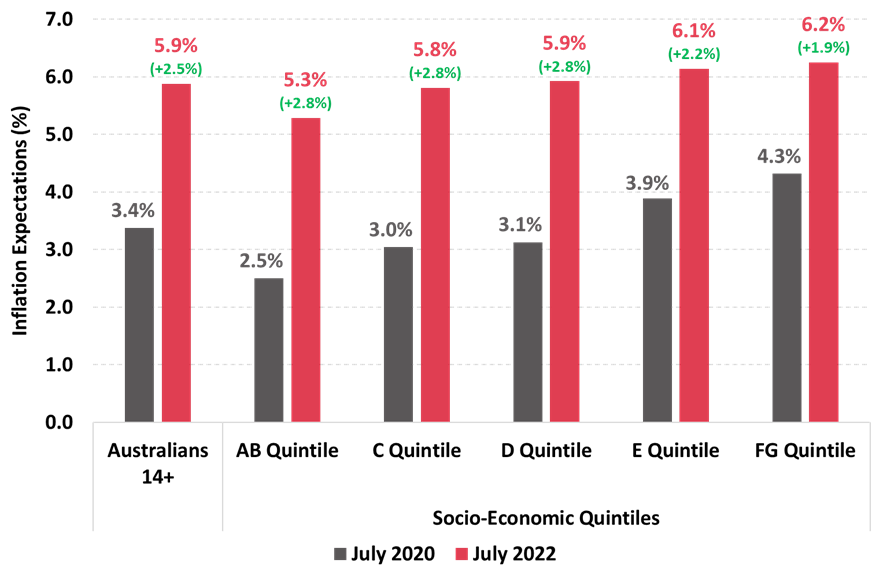

Inflation Expectations are highly correlated to Socio-Economic Quintile

A look at Inflation Expectations by socio-economic quintile shows large increases across the board since the measure hit record lows in mid-2020 during Victoria’s second wave.

Inflation Expectations are lowest for the top ‘AB Quintile’ at 5.3%, although this is up 2.8% points since mid-2020 – the equal largest increase of any socio-economic quintile.

Inflation Expectations are progressively higher for each subsequent socio-economic quintile including 5.8% (up 2.8% points) for the ‘C Quintile’, 5.9% (up 2.8% points) for the ‘D Quintile’, 6.1% (up 2.2% points) for the ‘E Quintile’ and are highest of all for the ‘FG Quintile’ at 6.2% (up 1.9% points).

The socio-economic quintiles* rank all respondents by considering their education level as well as the income and occupation of the respondent if they’re a full-time worker. See below for further details on how the socio-economic quintiles of the population are calculated.

Inflation Expectations by Socio-Economic Quintile: July 2020 cf. July 2022

Source: Roy Morgan Single Source: July 2020, n=5,803; July 2022, n=7,484. Base: Australians 14+.

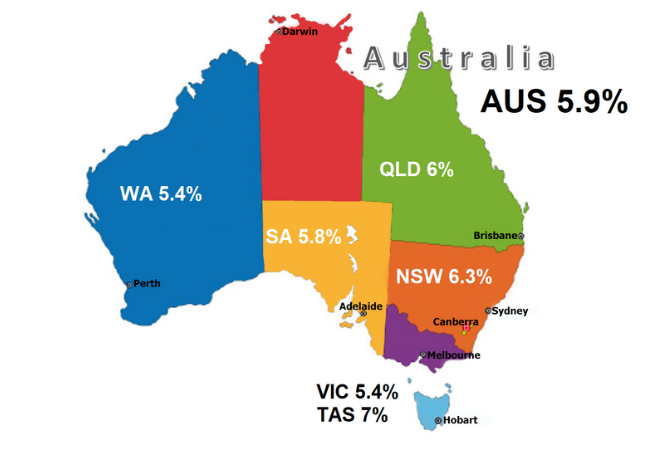

Inflation Expectations are again highest in Tasmania & NSW and lowest in Victoria & WA

On a State-based level Inflation Expectations were highest in Tasmania in July at 7%, far higher than any other State. Next highest was the largest State of NSW at 6.3% - also well above the national average.

Inflation Expectations in Queensland were just above the national average at 6% and just below the national average in South Australia at 5.8%.

In contrast, Inflation Expectations were once again lowest of all in both Western Australia and Victoria at only 5.4%.

Inflation Expectations Index long-term trend – Expected Annual Inflation in next 2 years

Source: Roy Morgan Single Source: Interviewing an average of 4,700 Australians aged 14+ per month (April 2010-July 2022).

See below for a comprehensive list of RBA interest rate changes during the time-period charted above.

Roy Morgan CEO Michele Levine says Inflation Expectations have hit a new eight-year high in July, up 0.2% points to 5.9% - the highest they’ve been since Augusvt 2012:

The data for the Inflation Expectations series is drawn from the Roy Morgan Single Source which has interviewed an average of 4,700 Australians aged 14+ per month over the last decade from April 2010 – July 2022 and includes interviews with 7,484 Australians aged 14+ in July 2022.

*Socio-Economic Status Quintiles

Each respondent is given a score up to 60 according to their status in each of the following categories:

1. EDUCATION LEVEL OF RESPONDENT

There are twelve levels of education. A score of 5 is given to those who completed only some primary school, 10 to those who finished primary school, and so on up to 60 for those who have a degree or post-graduate degree.

2. INCOME OF RESPONDENT (if respondent is a full-time worker)

There are eighteen income levels. A similar scoring procedure is used giving 2 to those in the lowest income group, up to 60 to those in the highest income group.

3. OCCUPATION OF RESPONDENT (if respondent is a full-time worker)

There are twelve occupation levels. Again, each level is scored at approximately 5-point intervals. Professional people receive the highest score. Note - if the respondent is not a full-time worker, then the status of the main income earner is considered.

The respondent’s scores for each of the three categories are then tallied to give a score out of 180.

We then look at the frequency distribution of the scores and divide the population into five even groups of 20%, i.e. quintiles.

The AB quintile is the highest level - people in this quintile have the highest scores.

Approximate breakdowns are:

Score

154+ - 5th or AB quintile

126 – 153 - 4th or C quintile

104 – 125 - 3rd or D quintile

81 – 103 - 2nd or E quintile

11 – 80 - 1st or FG quintile

Note - if the respondent is not a full-time worker, then the status of the main income earner is considered.

The questions used to calculate the Monthly Roy Morgan Inflation Expectations Index.

1) Prices: “During the next 2 years, do you think that prices in general will go up, or go down, or stay where they are now?”

2a) If stay where they are now: “Do you mean that prices will go up at the same rate as now or that prices in general will not go up during the next 2 years?

2b) If go up or go down: “By about what per cent per year do you expect prices to (go up/ go down) on average during the next 2 years?”

3) “Would that be (x%) per year, or is that the total for prices over the next 2 years?”

The Roy Morgan Inflation Expectations Index is a forward-looking indicator unlike the Consumer Price Index (CPI) and is based on continuous (weekly) measurement, and monthly reporting. The Roy Morgan Inflation Expectations Index is current and relevant.

| Monthly Roy Morgan Inflation Expectations Index (2010 – 2022) | |||||||||||||

| Year | Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | Yearly

Average |

| 2010 | n/a | n/a | n/a | 5.9 | 5.8 | 5.5 | 5.6 | 5.4 | 5.5 | 5.8 | 5.6 | 5.8 | 5.7 |

| 2011 | 6.6 | 6.4 | 6.4 | 6.2 | 6.1 | 6.2 | 6.1 | 5.8 | 5.7 | 5.8 | 5.5 | 5.5 | 6.0 |

| 2012 | 5.4 | 5.5 | 5.9 | 5.9 | 6.0 | 6.2 | 5.9 | 5.9 | 5.8 | 5.7 | 5.6 | 5.4 | 5.8 |

| 2013 | 5.2 | 5.1 | 5.3 | 4.9 | 5.2 | 4.9 | 5.3 | 5.0 | 4.8 | 4.9 | 4.8 | 5.0 | 5.0 |

| 2014 | 5.1 | 5.2 | 5.2 | 5.1 | 5.1 | 5.3 | 5.0 | 4.8 | 5.0 | 4.8 | 4.9 | 4.4 | 5.0 |

| 2015 | 4.4 | 4.3 | 4.5 | 4.5 | 4.2 | 4.4 | 4.4 | 4.5 | 4.5 | 4.2 | 4.4 | 4.5 | 4.5 |

| 2016 | 4.3 | 4.2 | 4.2 | 4.2 | 4.0 | 4.0 | 4.1 | 3.9 | 4.1 | 4.1 | 3.9 | 4.2 | 4.1 |

| 2017 | 4.5 | 4.4 | 4.4 | 4.4 | 4.3 | 4.2 | 4.3 | 4.5 | 4.4 | 4.5 | 4.5 | 4.5 | 4.4 |

| 2018 | 4.5 | 4.4 | 4.3 | 4.5 | 4.3 | 4.5 | 4.3 | 4.3 | 4.3 | 4.5 | 4.3 | 4.2 | 4.4 |

| 2019 | 4.2 | 4.0 | 4.0 | 3.7 | 4.1 | 3.8 | 4.1 | 3.9 | 4.0 | 4.1 | 3.9 | 4.0 | 4.0 |

| 2020 | 3.9 | 4.0 | 4.0 | 3.6 | 3.3 | 3.2 | 3.4 | 3.2 | 3.3 | 3.5 | 3.4 | 3.6 | 3.5 |

| 2021 | 3.6 | 3.7 | 3.8 | 3.7 | 3.7 | 4.0 | 4.1 | 4.3 | 4.5 | 4.8 | 4.9 | 4.8 | 4.2 |

| 2022 | 4.9 | 5.1 | 5.8 | 5.5 | 5.3 | 5.7 | 5.9 | 5.5 | |||||

| Monthly Average |

4.7 | 4.7 | 4.8 | 4.8 | 4.7 | 4.8 | 4.8 | 4.6 | 4.7 | 4.7 | 4.6 | 4.7 | 4.8 |

| Overall Roy Morgan Inflation Expectations Average: 4.7 | |||||||||||||

RBA interest rates changes during the time-period measured: 2010-2020.

RBA – Interest rate increasing cycle (2010):

2010

April 2010: +0.25% to 4.25%; May 2010: +0.25% to 4.75%, November 2010: +0.25% to 5%.

RBA – Interest rate cutting cycle (2011-2013, 2015-2016 & 2019-2020):

2011

November 2011: -0.25% to 4.5%; December 2011: -0.25% to 4.25%.

2012

May 2012: -0.5% to 3.75%; June 2012: -0.25% to 3.5%; October 2012: -0.25% to 3.25%;

December 2012: -0.25% to 3%.

2013

May 2013: -0.25% to 2.75%; August 2013: -0.25% to 2.5%.

2014

There were no RBA interest rate changes during 2014.

2015

February 2015: -0.25% to 2.25%; May 2015: -0.25% to 2%.

2016

May 2016: -0.25% to 1.75%; August 2016: -0.25% to 1.5%.

2017

There were no RBA interest rate changes during 2017.

2018

There were no RBA interest rate changes during 2018.

2019

June 2019: -0.25% to 1.25%; July 2019: -0.25% to 1%; October 2019: -0.25% to 0.75%.

2020

March 4, 2020: -0.25% to 0.5%, March 20, 2020: -0.25% to 0.25% & November 6, 2020: -0.15% to 0.10%.

RBA – Interest rate increasing cycle (2022):

2022

May 2022: +0.25% to 0.35%, June 2022: +0.5% to 0.85%; July 2022: +0.5% to 1.35%; August 2022: +0.5% to 1.85%.

For comments or more information please contact:

Roy Morgan - Enquiries

Office: +61 (03) 9224 5309

askroymorgan@roymorgan.com

Margin of Error

The margin of error to be allowed for in any estimate depends mainly on the number of interviews on which it is based. Margin of error gives indications of the likely range within which estimates would be 95% likely to fall, expressed as the number of percentage points above or below the actual estimate. Allowance for design effects (such as stratification and weighting) should be made as appropriate.

| Sample Size | Percentage Estimate |

| 40% – 60% | 25% or 75% | 10% or 90% | 5% or 95% | |

| 1,000 | ±3.0 | ±2.7 | ±1.9 | ±1.3 |

| 5,000 | ±1.4 | ±1.2 | ±0.8 | ±0.6 |

| 7,500 | ±1.1 | ±1.0 | ±0.7 | ±0.5 |

| 10,000 | ±1.0 | ±0.9 | ±0.6 | ±0.4 |

| 20,000 | ±0.7 | ±0.6 | ±0.4 | ±0.3 |

| 50,000 | ±0.4 | ±0.4 | ±0.3 | ±0.2 |