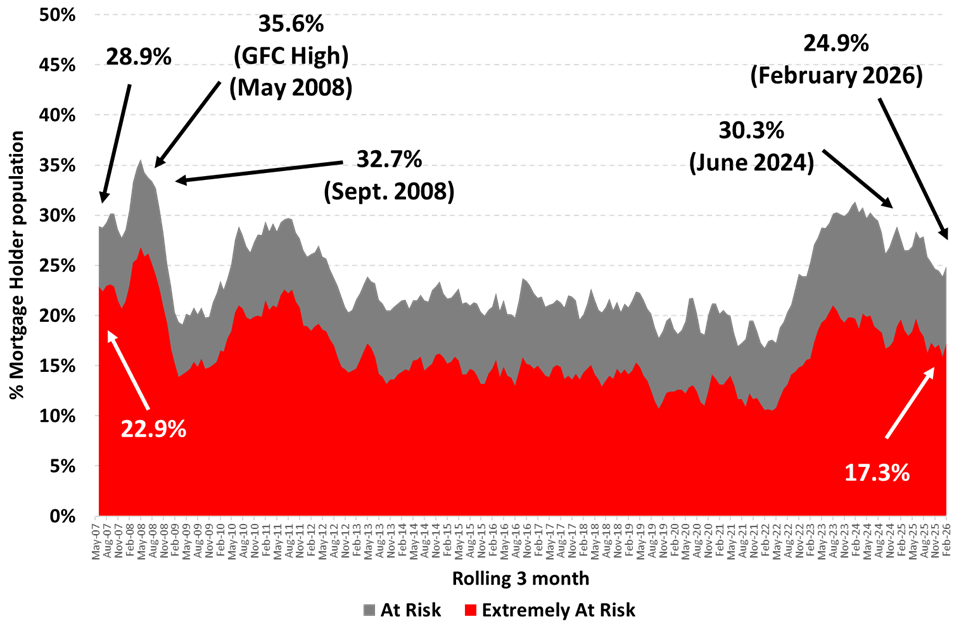

Risk of mortgage stress up by 1% point in February after the Reserve Bank raises interest rates

New research from Roy Morgan shows 24.9% of mortgage holders ‘At Risk’ of ‘mortgage stress’ in the three months to February 2026, up 1% point from January 2026, after the Reserve Bank raised interest rates in early February by +0.25% to 3.85%.

This is the first increase in mortgage stress since August 2025, the last time the Reserve Bank cut interest rates. The record high of 35.6% of mortgage holders in mortgage stress was reached back in mid-2008.

232,000 fewer ‘At Risk’ of mortgage stress compared to a year ago despite rate increase

The number of Australians ‘At Risk’ of mortgage stress has decreased by 232,000 compared to a year ago when the RBA began a cycle of interest rate cuts which lowered rates by a total of 0.75% from 4.35% in February 2025 to 3.6% from August 2025 through to January 2026 – when the RBA raised rates.

The number of Australians considered ‘Extremely At Risk’, is now numbered at 918,000 (17.3% of mortgage holders) which is just above the long-term average over the last two decades of 16.3%.

Mortgage Stress – % of Owner-Occupied Mortgage-Holders

Source: Roy Morgan Single Source (Australia), average interviews per 3 month period April 2007 – Feb 2026, n=2,886.

Base: Australians 14+ with owner occupied home loan.

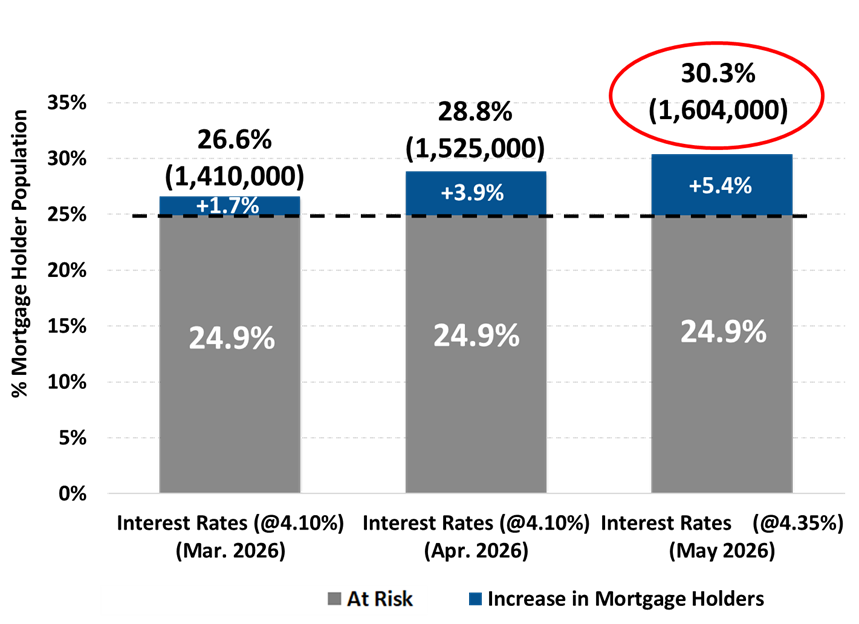

Mortgages ‘At Risk’ is set to rise if the Reserve Bank increases interest rates to 4.35% in May

The Reserve Bank raised interest rates in February, up +0.25% to 3.85% and again in mid-March by another +0.25% to 4.1%. These increases were due to a doubling in the official ABS annual inflation which hit a low of 1.9% in the year to June 2025, and has since doubled – the latest figure is 3.8% in the year to January 2026.

Because of this, Roy Morgan modelled the impact of the RBA increasing interest rates at its March 2026 meeting (+0.25% to 4.1%) and again if the RBA increases rates again in May 2026 (+0.25% to 4.35%).

In February, 24.9% of mortgage holders (1,317,000) were considered ‘At Risk’. The RBA’s decision to increase interest rates in March increased the share of mortgage holders ‘At Risk’ to an estimated 26.6% (up 1.7% points from February) and equivalent to 1,410,000 (up 93,000).

The share of mortgage holders considered ‘At Risk’ is forecast to rise to 28.8% (up 3.9% points) in April and equivalent to 1,525,000 mortgage holders, up 208,000 from now.

If the RBA raises rates in May by 0.25% to 4.35% the share of mortgage holders ‘At Risk’ would increase to 30.3% – up 5.4% points from now and equivalent to 1,604,000 mortgage holders, up 287,000 from now.

Mortgage Risk projections based on an interest rate increase in May 2026 by 0.25%

Source: Roy Morgan Single Source (Australia), December 2025 – February 2026, n=3,385.

Base: Australians 14+ with owner occupied home loan.

How are mortgage holders considered ‘At Risk’ or ‘Extremely At Risk’ determined?

Roy Morgan considers the risk of ‘mortgage stress’ among mortgage holders in two ways:

Mortgage holders are considered ‘At Risk’ [1] if their mortgage repayments are greater than a certain percentage of household income – depending on income and spending.

Mortgage holders are considered ‘Extremely at Risk’ [2] if even the ‘interest only’ is over a certain proportion of household income.

Unemployment is the key factor which has the largest impact on income and mortgage stress

It is worth understanding that Roy Morgan uses a conservative forecasting model, essentially assuming all other factors apart from interest rates remain the same.

The latest Roy Morgan unemployment estimates show over one-in-five Australian workers are either unemployed or under-employed – 3,613,000 (22.2% of the workforce); (In February, overall Australian unemployment and under-employment was at 3.61 million, ‘Real unemployment’ at 1.72 million).

Although the Reserve Bank’s decision to cut interest rates three times last year had a positive impact and helped lower mortgage stress, the fact remains the greatest impact on an individual, or household’s, ability to pay the mortgage is not interest rates, it’s if they lose their job or main source of income.

And since then, the Reserve Bank has started 2026 with two straight interest rate increases in February and March – reversing the last two of its interest rate cuts in 2025 already. In addition, the intense economic uncertainty provided by the renewed conflict in the Middle East is already pushing energy prices higher and will add further pressure to inflation in the months ahead.

Michele Levine, CEO Roy Morgan, says the Reserve Bank’s decision to raise interest rates in early February has led to the first increase in mortgage stress since mid-2025:

“The latest Roy Morgan data shows mortgage stress in February 2026 rising off a three-year low, up 1% point from January to 24.9% of mortgage holders (equivalent to 1,317,000) ‘At Risk’. However, despite this increase, mortgage stress is still 3% points below the level in August 2025.

“The rise in mortgage stress was caused by the Reserve Bank’s decision to raise interest rates by +0.25% to 3.85% in early February which followed a doubling in the rate of official inflation from 1.9% in the year to June 2025 to 3.8% in the year to January 2026.

“Following on from this rate increase the Reserve Bank again raised interest rates in mid-March by +0.25% to 4.1%. In addition, Roy Morgan has modelled another potential interest rate increase in May of +0.25% to 4.35%. If the RBA does raise interest rates again the level of mortgage stress would rise to 1,604,000 (30.3% of mortgage holders) by May 2026.

‘However, the outbreak of conflict in the Middle East in late February, following the Israeli and US attacks on Iran, has introduced a considerable amount of uncertainty into global economic forecasts. Given this uncertainty Australia is set to face a wave of inflation prompted by soaring energy prices, or an economic slowdown due to rising energy prices impacting demand elsewhere in the economy.

“Since the conflict in the Middle East began ANZ-Roy Morgan Inflation Expectations have increased significantly, up 1.6% points in a matter of weeks to a record high of 6.9%, and at the same time, average retail petrol prices have increased by over 70 cents per litre (+43.3%) to a new record high of $2.38 – both strong indications of high inflation on the way.

“The high degree of uncertainty about how the conflict in the Middle East has introduced an additional, and volatile, variable into the decision making of the Reserve Bank over the next few months – although the Albanese Government has been quick to provide assurances that Australia is well supplied with energy over the next few weeks at least.

“Finally, it is important to appreciate that interest rates are only one of the variables that determines whether a mortgage holder is considered ‘At Risk’ – the largest impact on whether a borrower falls into the ‘At Risk’ category is related to household income – which is directly related to employment.

“The employment market has been strong over the last four years (Roy Morgan estimates show 1.3 million new jobs have been created since the Albanese Government was elected in May 2022) and this has provided support to household incomes which have helped to moderate levels of mortgage stress despite interest rates increasing rapidly since May 2022 .”

[1] "At Risk" is based on those paying more than a certain proportion of their after-tax household income (25% to 45% depending on income and spending) into their home loan, based on the appropriate Standard Variable Rate reported by the RBA and the amount they initially borrowed.

[2] "Extremely at Risk" is also based on those paying more than a certain proportion of their after-tax household income (25% to 45% depending on income and spending) into their home loan, based on the Standard Variable Rate set by the RBA and the amount now outstanding on their home loan.

These are the latest findings from Roy Morgan’s Single Source Survey, based on in-depth interviews conducted with over 60,000 Australians each year including over 10,000 owner-occupied mortgage-holders.

To learn more about Roy Morgan’s mortgage data, call (+61) (3) 9224 5309 or email askroymorgan@roymorgan.com. Please click on this link to the Roy Morgan Online Store.

About Roy Morgan

Roy Morgan is Australia’s largest independent Australian research company, with offices in each state, as well as in the U.S. and U.K. A full-service research organisation, Roy Morgan has over 80 years’ experience collecting objective, independent information on consumers.

Margin of Error

The margin of error to be allowed for in any estimate depends mainly on the number of interviews on which it is based. Margin of error gives indications of the likely range within which estimates would be 95% likely to fall, expressed as the number of percentage points above or below the actual estimate. Allowance for design effects (such as stratification and weighting) should be made as appropriate.

| Sample Size | Percentage Estimate |

| 40% – 60% | 25% or 75% | 10% or 90% | 5% or 95% | |

| 1,000 | ±3.0 | ±2.7 | ±1.9 | ±1.3 |

| 5,000 | ±1.4 | ±1.2 | ±0.8 | ±0.6 |

| 7,500 | ±1.1 | ±1.0 | ±0.7 | ±0.5 |

| 10,000 | ±1.0 | ±0.9 | ±0.6 | ±0.4 |

| 20,000 | ±0.7 | ±0.6 | ±0.4 | ±0.3 |

| 50,000 | ±0.4 | ±0.4 | ±0.3 | ±0.2 |