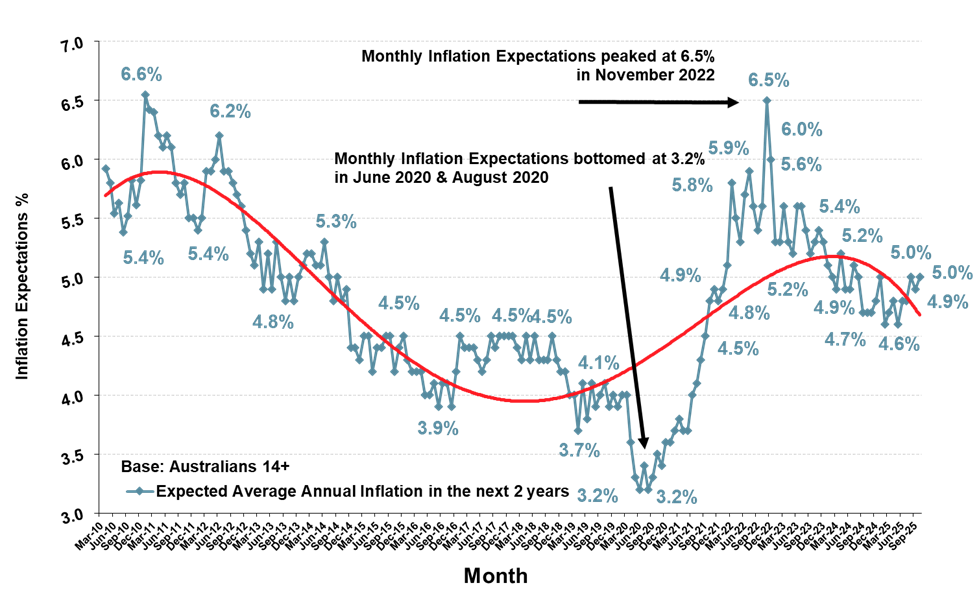

ANZ-Roy Morgan Inflation Expectations are at 5.4% in late November – up 0.4% points from the month of October

The weekly ANZ-Roy Morgan Inflation Expectations hit a near two-year high at 5.4% for the week of November 17-23, 2025, up 0.4% points from the full month of October – the highest the index has been on a weekly basis since December 2023.

A look at monthly Inflation Expectations for October 2025 shows the measure at 5.0% for the month – up 0.1% points from the prior month of September, but since then inflationary pressures have increased.

Looking back over the last six months, since early June 2025, weekly Inflation Expectations have moved in a band of 4.7% - 5.4% and averaged 5.0%. In addition, the latest information on weekly Inflation Expectations is available to view each week in the Roy Morgan Weekly Update video on YouTube.

Monthly Inflation Expectations Index long-term trend – Expected Annual Inflation in next 2 years

Source: Roy Morgan Single Source: Interviewing an average of 4,900 Australians aged 14+ per month (April 2010 – Oct. 2025).

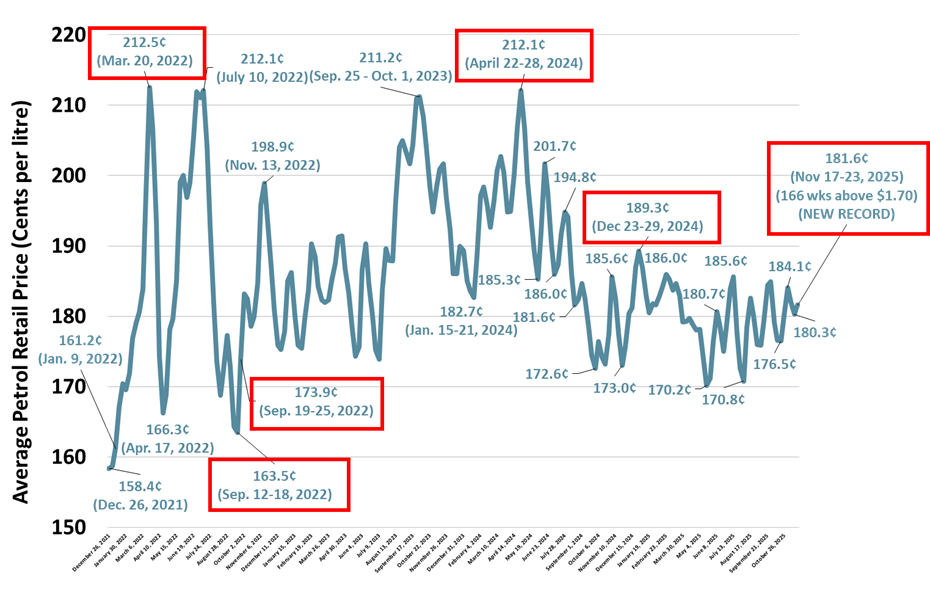

Average retail petrol prices dropped three cents per litre to $1.78 per litre in October

During October, average retail petrol prices dropped three cents to $1.78 per litre – returning to their average price in August 2025. Average retail petrol prices started the month of October at $1.79 per litre and dropped during mid-October before increasing and ending the month on a high of $1.80 per litre. Since the end of October, average petrol prices have continued to increase so far in November.

Looking longer-term, average retail petrol prices have now been at, or above, $1.70 per litre for a record 166 straight weeks, equivalent to over three years uninterrupted, since mid-September 2022.

More recently, average retail petrol prices hit near three-year lows in May but then rebounded in June and July. This recent volatility is reflected in the weekly Inflation Expectations of Australians which have moved in a band of 0.7% between 4.7-5.4% during the last six months from June - November. On a weekly level, Inflation Expectations have increased 13 times, decreased nine times, and been unchanged four times.

The reduction in petrol prices earlier this year clearly lessened inflation pressures and was no doubt a factor for the Reserve Bank behind its decision to cut interest rates in February, May and early August. However, there has been renewed strength in petrol prices in recent weeks and months, and in turn inflationary pressures have re-accelerated across the economy.

Australian average retail petrol prices (cents per litre) weekly: 2021 – 2025

Source: Australian Institute of Petroleum (AIP) weekly reports: https://www.aip.com.au/pricing/weekly-prices-reports.

The latest official ABS quarterly annual CPI estimate at 3.2% for the year to September 2025 is now above the Reserve Bank’s preferred target range of 2-3% over the course of the economic cycle. This is the first time quarterly estimates of inflation have breached the upper limit of the Reserve Bank’s preferred target range of 2-3% over the course of the economic cycle for over a year since June 2024 (3.8%).

The increase in official estimates of inflation led to the Reserve Bank’s decision to leave interest rates unchanged for its last two meetings in October and November 2025. This is the first time so far in 2025 the Reserve Bank has left interest rates unchanged at two consecutive meetings.

The next ABS Monthly CPI estimate for October 2025 is due to be released this week on Wednesday.

Inflation Expectations were again highest in Western Australia and Queensland at over 5%

A look at Monthly Inflation Expectations on a State-based level for October shows increases around Australia in all six States and for a third straight month highest in Queensland (up 0.4% points to 5.4%) and Western Australia (up 0.2% points to 5.3%).

Inflation Expectations also increased in Tasmania (up 0.3% points to 5.2%), in South Australia (up 0.5% points to 5.1%), New South Wales (up 0.1% points to 5.0%) and Victoria (up 0.1% points to 4.9%), but still the lowest Inflation Expectations of any State.

Inflation Expectations in Country Areas were unchanged at 5.2% in October but increased by 0.2% points to 4.9% in Capital Cities.

Roy Morgan CEO Michele Levine says weekly Inflation Expectations were at a near two-year high of 5.4% in late November, up 0.4% points from the October estimate of 5.0%, and emblematic of building inflationary pressures in the Australian economy:

“ANZ-Roy Morgan Inflation Expectations in Australia have continued to increase so far in November and are now at 5.4%, up 0.4% points from the full month of October (5.0%). Inflation Expectations in the month of October were up 0.1% points from the month of September (4.9%).

“These results show that Inflation Expectations are on track to increase for a second consecutive month in November – the first back-to-back monthly increases since April 2025 and look likely to reach their highest level on a monthly basis since December 2023.

“The increase in Inflation Expectations in October, and so far during November, is no surprise with inflationary pressures driven by energy prices clearly a key factor. For instance, the average retail petrol price is on track to hit an eight-month high above $1.80 per litre in November.

“The rise in Inflation Expectations, and average retail petrol prices, has been matched by a sustained rise in the official ABS Inflation from a low of 1.9% in June 2025, up to 2.8% in July 2025, 3.0% in August 2025, and 3.5% in September 2025 – the highest since July 2024 (3.5%).

“The sharp rise in inflationary pressures in the broader economy during the last three months – rising by 1.6% points since June – has led to the Reserve Bank’s decision to leave interest rates unchanged at 3.6% at each of its last two monthly meetings in October and November.

“Looking forward, as long as inflationary pressures in the economy remain elevated the Reserve Bank is not likely to cut interest rates again any time soon, and some commentators are now suggesting the next move in official interest rates may even be up.”

See below for a comprehensive list of RBA interest rate changes during the time-period charted above.

The data for the Inflation Expectations series is drawn from the Roy Morgan Single Source which has interviewed an average of around 5,300 Australians aged 14+ per month over the last decade from November 2015 – October 2025 and includes interviews with 5,099 Australians aged 14+ in October 2025.

For comments and information about Roy Morgan’s Inflation Expectations data, please contact:

Roy Morgan Enquiries

Office: +61 (3) 9224 5309

askroymorgan@roymorgan.com

About Roy Morgan

Roy Morgan is Australia’s largest independent Australian research company, with offices in each state, as well as in the U.S. and U.K. A full-service research organisation, Roy Morgan has over 80 years’ experience collecting objective, independent information on consumers.

Margin of Error

The margin of error to be allowed for in any estimate depends mainly on the number of interviews on which it is based. Margin of error gives indications of the likely range within which estimates would be 95% likely to fall, expressed as the number of percentage points above or below the actual estimate. Allowance for design effects (such as stratification and weighting) should be made as appropriate.

| Sample Size | Percentage Estimate |

| 40% – 60% | 25% or 75% | 10% or 90% | 5% or 95% | |

| 1,000 | ±3.0 | ±2.7 | ±1.9 | ±1.3 |

| 5,000 | ±1.4 | ±1.2 | ±0.8 | ±0.6 |

| 7,500 | ±1.1 | ±1.0 | ±0.7 | ±0.5 |

| 10,000 | ±1.0 | ±0.9 | ±0.6 | ±0.4 |

| 20,000 | ±0.7 | ±0.6 | ±0.4 | ±0.3 |

| 50,000 | ±0.4 | ±0.4 | ±0.3 | ±0.2 |